A groundbreaking study reveals the

devastating financial toll of undiagnosed dementia, showing household

wealth can plummet by half in the eight years before official diagnosis.

This critical window, marked by subtle cognitive decline and increased

vulnerability to exploitation, often goes unnoticed by families until

significant damage occurs.

By Garret Reich, Senior Project Manager at The Financial Brand

Source: MIT and AARP

Why we picked it: The World Health Organization in 2023 estimated there are some 55 million people globally that live with dementia, and that could nearly triple by 2050 — only a few decades later. This poses some massive strategic issues for financial institutions who want to build familial relationships with customers and members.

Executive Summary

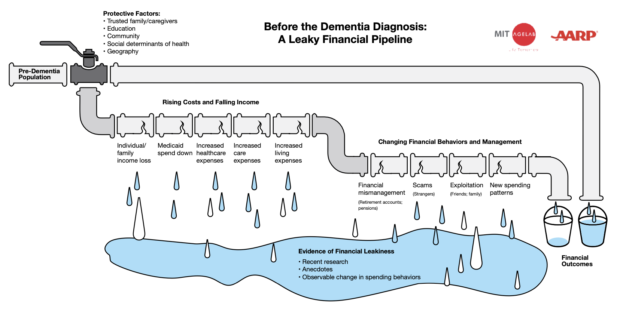

Money begins vanishing from bank accounts years before a dementia diagnosis, according to groundbreaking new research from MIT and AARP. A 2023 study found that households see their wealth plummet by more than half in the eight years leading up to a dementia diagnosis — from $217,000 down to just $104,000 — highlighting a devastating but largely invisible financial toll.

As cognitive decline subtly begins, individuals start making poor financial decisions and become more vulnerable to exploitation, while family members remain unaware of the growing crisis. This pre-diagnosis phase represents a critical window where intervention could help protect life savings, but most families miss the warning signs until significant damage is done.

Key Takeaways:

- Financial impacts can begin up to six to eight years before an official dementia diagnosis, with missed payments and declining credit scores serving as early red flags.

- Adult children often face severe financial strain trying to help parents, with many taking out personal loans or reducing work hours to provide care.

- Artificial intelligence is making scams increasingly sophisticated, with new technology allowing fraudsters to mimic family members’ voices in elaborate schemes.

- Early diagnosis appears to help prevent major wealth losses, suggesting that proactive screening could provide vital protection for family finances.

What we liked about the report: The consumer perspectives went a long way to provide additional context into why this is such a poignant issue. Lots of quotes and personal stories throughout.

What we didn’t: The stories were very helpful, but were also sometimes too much. The narrative was clear from the onset, but it doesn’t have to be as heavily emphasized throughout the rest of the report.

The Scale of the Crisis

Nearly one in 10 adults over age 65 have diagnosable dementia, with more than twice that number showing early signs of mild cognitive impairment (MCI). This creates a large vulnerable population at risk of financial exploitation and mismanagement.

Recent studies paint a stark picture of how cognitive decline erodes financial capability. A 2020 analysis found that individuals begin missing more payments and seeing credit scores drop up to six years before diagnosis. The financial impact appears unique to dementia — similar patterns don’t emerge with other health conditions like arthritis or heart disease.

"The financial services industry is very aware of this problem," says Lauren Hersch Nicholas, a health economist at the University of Colorado School of Medicine, noting that 84% of financial advisors report encountering cognitively impaired clients.

Just because they are aware of the issue, however, doesn’t mean that financial institutions are yet equipped with the processes and proactive measures needed to mitigate the problem before it becomes one.

The Impact on Families

For family members watching savings evaporate, the experience can be emotionally and financially devastating. Many adult children find themselves draining their own resources trying to help parents who don’t recognize they need assistance.

"I had to bail her out using my own finances," says Reagan, who took out $10,000-15,000 in personal loans to cover her mother’s expenses while also trying to put her own children through college. "My credit is really great, so I am able to take out some personal loans and help her."

The pre-diagnosis phase proves especially challenging because cognitive decline often coincides with individuals becoming more secretive about finances. Adult children describe frustrating battles trying to gain access to accounts or even basic information about their parents’ assets.

"She was very secretive and kept her money separate," says Cathy about her mother. "She didn’t trust her children around her checking account." This isolation made it nearly impossible for family to intervene before significant losses occurred.

For some families, the financial strain extends beyond immediate household members. Londyn, caring for both her grandmother and infant daughter, had to postpone returning to work. "My plan was to go back to work, but my mother needed help," she explains. "I kind of took a hit in a sense… I have to budget a bit more. Entertainment money for my kids is a bit smaller."

New Threats in the Digital and Regulatory Ages

While traditional financial risks persist, emerging technologies create additional dangers. Artificial intelligence now allows scammers to create highly convincing fraud schemes, including the ability to clone voices of family members.

"Generative AI lets scammers be so good," warns Nicholas. "You can have voices of family members say ‘I’ve been kidnapped’ instead of some muffled voice in the background."

Jilenne Gunther, National Director of AARP’s BankSafe Initiative, notes that while their program has prevented over $300 million in elder fraud, this represents just "the tip of the iceberg" given annual losses of $28.3 billion to senior scams.

The legal system often struggles to balance protection with autonomy. Nina Kohn, Professor of Law at Syracuse University, explains that advance planning isn’t always effective: "Advance planning done when people are cognitively intact isn’t of much use when institutions are asking for new forms — new power of attorney — when dementia is now occurring."

Some states are experimenting with new approaches. Maine allows older adults to reverse financial transactions made with someone in a position of trust, while Illinois enables those over 60 to seek damages from people who use deception while acting in positions of confidence.

Mike Festa, State Director of AARP Massachusetts, emphasizes the delicate balance required: "If that person is competent, they have a right to make bad decisions." This creates challenges for protective services trying to prevent exploitation while respecting individual autonomy.

The Vicious Circle of Cognitive Decline and Financial Losses

Research suggests the relationship between cognitive decline and financial losses can be circular. While cognitive issues may trigger financial problems, severe financial setbacks — especially those involving loss of housing — can accelerate cognitive decline.

Lindsay Kobayashi, Professor of Epidemiology at the University of Michigan, describes this as a potential "vicious cycle" between financial and cognitive health losses. Her research indicates that major financial shocks can lead to cognitive impairment, particularly in countries with weaker social safety nets.

The research points to several promising avenues for protecting vulnerable seniors and their assets. Earlier screening and diagnosis appear to help prevent major wealth losses. Financial institutions are developing AI tools to flag suspicious patterns, while healthcare providers are working to improve early detection of cognitive decline.

Brain health maintenance through social engagement, cognitive stimulation, stress management, exercise and proper diet may help protect both cognitive and financial wellbeing. The financial services industry is also adapting, with initiatives to train advisors on recognizing signs of impairment and implementing protective measures.

Proactive Prescriptions

While the challenges are substantial, symposium participants emphasized reasons for hope. "I want to leave with a message of hope," says Brent Forester of Tufts University School of Medicine, urging a "focus on how there’s so much more that people with dementia can still do, that’s meaningful to them and their family members."

However, addressing these challenges requires coordinated effort across sectors. As MIT AgeLab founder Joseph Coughlin says, "this issue is too big and too important to say it’s a government issue or business issue alone. Before there is action, before you seek help, there needs to be awareness."

The study’s findings make clear that waiting until an official dementia diagnosis to take protective measures means missing a crucial intervention window. For families hoping to preserve hard-earned savings, understanding and acting on early warning signs could make all the difference.

Grace, an expert in public health policy who shared her family’s experience with exploitation, emphasizes the urgency: "We need to get to work now." With seventeen years typically required for research findings to become standard practice, there’s no time to waste in implementing protective measures for vulnerable seniors and their finances.

An Action Plan for Banks

Financial institutions stand at a critical intervention point in addressing dementia’s hidden financial toll. Banks witnessing these patterns firsthand can implement several protective measures:

- Deploy AI-powered monitoring systems to detect unusual transaction patterns, missed payments, and potential exploitation

- Train customer-facing staff to recognize subtle cognitive decline indicators and respond appropriately

- Implement streamlined processes for trusted contact authorization that balance protection with privacy

- Offer "view-only" account access options for family members concerned about declining financial management

- Develop specialized financial advisory services addressing cognitive aging’s unique challenges

- Create simplified account structures that minimize vulnerability while preserving customer autonomy

- Establish clear intervention protocols when suspicious activity is detected

- Partner with elder care and community organizations to build comprehensive support networks

- Design educational programs for both customers and families about financial protection during cognitive aging

Editor’s note: This article was prepared with AI language software and edited for clarity and accuracy by The Financial Brand editorial team.

Full Article & Source:

Dementia’s Hidden Cost: How Cognitive Decline Compounds Banking Errors and Enables Fraud

No comments:

Post a Comment